The Ultimate Singaporean Guide to CFDs (Contracts for Difference)

You know when your investment spidey senses kick in?

You watch the news, and suddenly there’s a voice in your head telling you that the price of something is about to surge? Maybe it is a tech giant releasing a new product, or some random commodity that is suddenly in hot demand because of a supply chain issue.

You stared at the few thousand dollars in your brokerage account thinking, "If I only had ten times this amount, I could make some serious money."

This is exactly where the seductive, fast, and often dangerous world of CFDs (Contracts for Difference) enters the chat.

It is the financial equivalent of trying to eat the entire buffet at a wedding; it looks glorious, you want everything, but if you bite off more than you can chew, you are going to end up with a very painful stomachache.

Many Singaporean investors hear the term and think it is some kind of magic bullet for wealth. Let me tell you right now: it is not. It is a high-octane tool that requires a level of discipline that would put a monk to shame. If you have ever wondered why some people make a killing while others lose their entire year-end bonus in an afternoon, this guide is for you.

TL;DR: Everything You Need to know about CFDs (Contracts for Difference)

- Definition: You are not buying the asset (like a share of Apple). You are betting on the price movement. If you are right, you win the difference. If you are wrong, you pay the difference.

- Leverage: Due to the ability to leverage, you can control a large position with a small amount of money (margin). In Singapore the maximum retail leverage is up to 20:1.

- The Danger: Leverage works both ways. You can amplify your gains, but you can also lose more than your initial deposit.

- More Cost: Watch out for overnight financing fees, spreads, and commissions.

What on Earth is a CFD?

Imagine you want to buy a pair of fancy sneakers that cost $500.

You don't actually want to wear them. You just think they will be worth $600 by the end of the week.

Instead of buying the physical shoes, storing them, and finding a buyer through Carousell, you and your friend make a deal

"If the price goes up to $600, you pay me $100. If it drops to $400, I pay you $100."

That, in a nutshell, is a CFD.

You do not own the underlying asset. You are entering a contract with a broker to exchange the difference in value between the price at the time you open the position and the price at the time you close it. You are essentially playing a game of "up or down" with the market, but with professional-grade tools.

How Do You Make Money (and Lose It)?

CFDs allow you to go "long" or "short." This is the part that makes most retail investors feel like they are gambling 大小 during Chinese New Year.

- Going Long: You think the price of an asset (like a gold commodity) will go up. You open a "Buy" position.

If the price rises, you close the position and pocket the difference. - Going Short: This is the magic of CFDs. You think the market is going to crash? You open a "Sell" position.

If the price goes down, you make money.

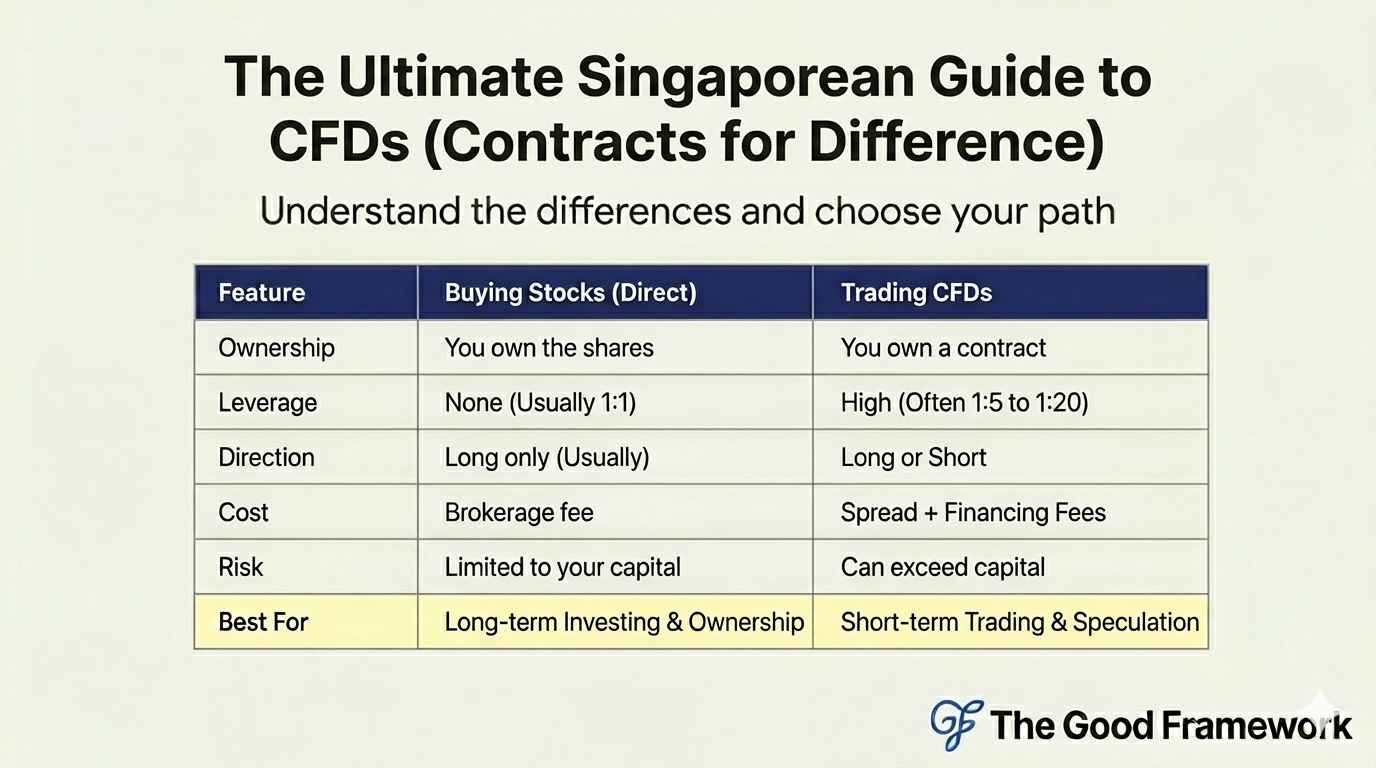

The Toolkit: A Simple Comparison

Winner: Stocks for long-term investors; CFDs for short-term speculation.

You make money when your prediction about the price movement is correct, multiplied by your leverage.

However, do take note of the "hidden" costs.

Every day you hold your position open, the broker charges you a "financing fee" because they are essentially lending you the money to hold that larger position.

The Singapore Context: Leverage, Rules, and Reality

If you are a resident in Singapore, the Monetary Authority of Singapore (MAS) keeps a very close eye on this. They know that leverage is a double-edged sword.

Leverage is Not Your Best Friend

In Singapore, MAS restricts the amount of leverage providers can offer retail investors. This is to prevent people from losing their entire BTO savings in a single, bad trade. Leverage allows you to control a position worth, say, $10,000 with only $1,000 of your own money (that is 1:10 leverage).

If the asset moves in your favuor by 5%, you don't make 5% on your $1,000. You actually make 50% profit ($500). While that sounds amazing, if it drops by 5%, you lose 50% of your capital too.

If it drops by 10%, you have lost more than your initial deposit. Some brokers will issue a "margin call," demanding you top up more money into your account immediately. If you are unable to do so, they close your position and you realise a total loss.

Regulations You Need to Know

Singapore is not the Wild West. MAS requires CFD providers to be licensed as Capital Markets Services (CMS) license holders. Always check the MAS Financial Institutions Directory before you deposit a single cent.

If a broker is not on the MAS Financial Institutions Directory, stay the F**k away from it.

Furthermore, there is the concept of "Negative Balance Protection." Many reputable brokers now offer this, which ensures that even in a chaotic market flash crash, you cannot lose more than what you have in your account.

Still, that is a cold comfort when your account balance hits zero. That is some hard-earned money gone right there.

Taxes and Costs

Singapore does not have a capital gains tax.

That is the good news. However, you need to be aware of the "spread." This is the difference between the buy price and the sell price. The broker makes their money here, and it is essentially a hidden cost of trading. You start every trade at a slight loss because of this spread.

Wait, How Do I Choose?

If you are still reading and thinking, "Okay, this sounds risky but I want to try," you need to be systematic.

- Pick a Regulated Provider: Do not use some offshore broker just because they offer 1:500 leverage. It is a trap. Stick to MAS-regulated entities.

- Start with a Demo Account: Most brokers offer practice accounts with virtual money. If you cannot make a profit with "fake" money, do not even think about using your real money.

- Define Your Strategy: Are you a day trader? A swing trader? You need a plan for when to get in, and more importantly, a plan for when to get out (Stop Loss).

- Use Stop-Loss Orders: This is non-negotiable. A stop-loss is an instruction to your broker to close the position automatically if the price hits a certain point. It is your emergency exit door. Use it.

The Verdict: Is It Worth It?

Let’s be honest. For 95% of Singaporeans, CFDs are not worth the stress.

If you are a working professional who is busy with your day job, trying to manage a BTO renovation, or worrying about your next career move, you do not have the time to watch the market 24/7. Markets move fast, and with leverage, you can get wiped out while you are stuck in a meeting or trying to order a kopi at the hawker centre.

However, if you are a disciplined investor, if you enjoy the technical side of trading, and if you treat it with the seriousness of a business instead of a casino, hen it can be a tool. But treat it like a sharp knife; it is very useful for a chef, but if you treat it like a toy, you will get cut.

A Final Thought: Your Wealth, Your Sanity

At the end of the day, your financial success is not defined by whether you can pull off a complex leveraged trade. It is defined by your ability to save, your consistency in investing in diversified assets, and your patience.

Disclaimer: I am just a friendly voice here to help you navigate the jargon. I am not a financial advisor. Trading CFDs involves significant risk of loss. Always do your own research or talk to a licensed financial advisor before making any investment decisions. Never trade with money you cannot afford to lose.