The Ultimate Guide to Investing in the Straits Times Index (STI) ETF

You have been working hard, and now you want your money to start doing the heavy lifting for you.

When it comes to investing, the Straits Times Index (STI) feels like the sensible, homegrown choice.

It is made up of companies that we are familiar with, from the bank where we keep our savings to the telco we use to doomscroll on the MRT.

But is it actually a good investment compared to the global giants?

Let us dive into the details.

TL;DR: The Bottom Line of Straits Times Index (STI)

- What is the Straits Times Index (STI)? The STI is an index representing the top 30 companies listed on the Singapore Exchange (SGX).

- The Big Picture: It is a defensive, dividend-heavy play, not a high-growth tech rocket ship.

- The Two Contenders: We have two main Exchange Trded Funds (ETFs)in Singapore: the SPDR STI ETF (SGX: ES3) and the Nikko AM Singapore STI ETF (SGX: G3B).

The STI vs The World: How Does It Stack Up?

Like every Asian parent, let us look at the performance of the STI vs the world.

When we look at the performance of various global indices over the last decade, the difference in returns is stark.

While the S&P 500 has experienced a massive rally, the STI's performance remained relatively stable, often acting as a defensive play rather than a high-growth engine.

(Note: Data reflects annual price returns based on historical market trends; past performance is not an indicator of future results.)

Why the STI is Often Called a "Safe Haven"?

You might notice that in years of global turmoil, such as during heightened US-Iran geopolitical tensions or global pandemic-induced volatility, the STI often performs with lower beta compared to high-growth tech indices.

Because the STI is heavily weighted towards banking and real estate investment trusts (REITs), it tends to be more resilient during turbulent times.

While you might not see the explosive growth of a tech-heavy index, you are generally buying into stable, dividend-paying giants.

It is the financial equivalent of a solid plate of chicken rice: it might not be one of those fancy Michelin-starred meal, but it is reliable and keeps you going.

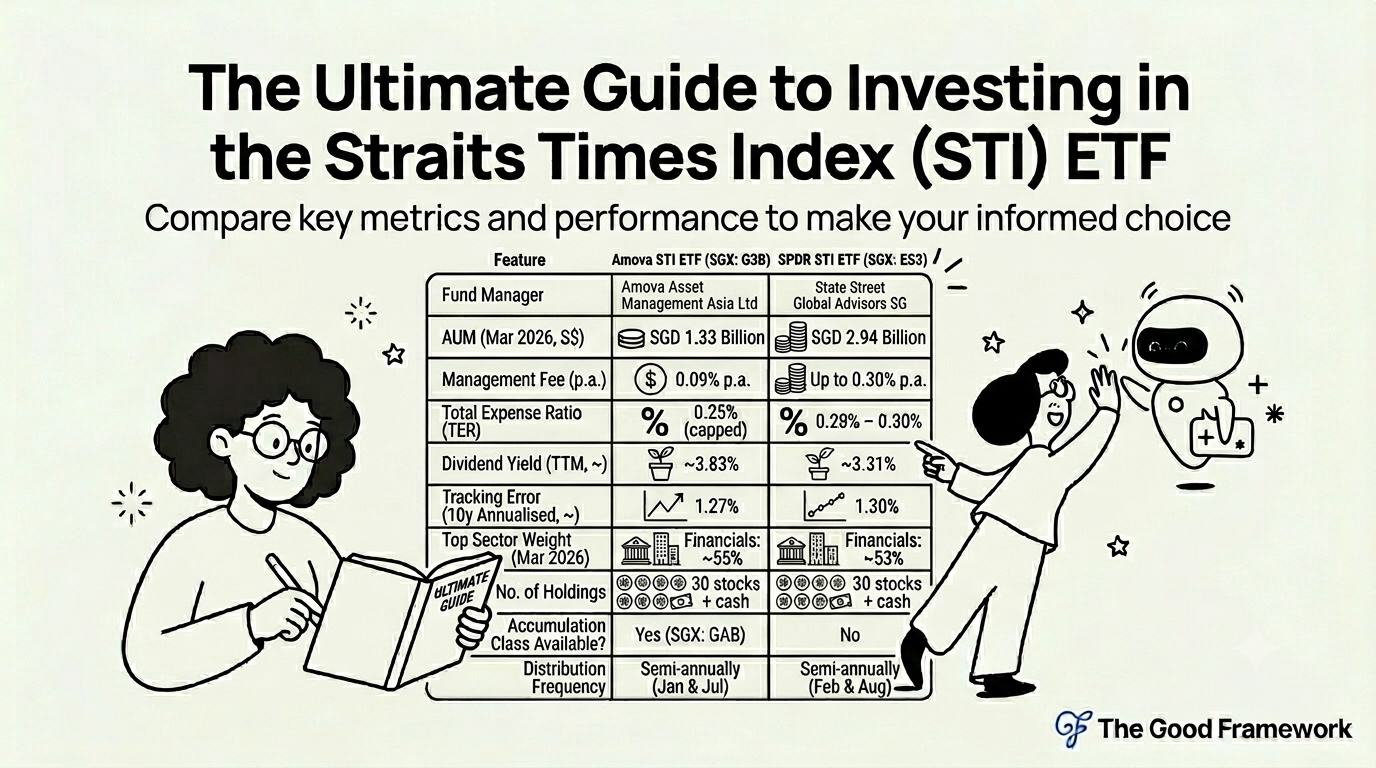

Comparing the Two STI ETFs: Amova Singapore STI ETF vs SPDR STI ETF

You cannot buy "the index" directly. Instead, you need to buy an Exchange Traded Fund (ETF) that tracks the index. As of late 2025, the fund formerly known as the Nikko AM Singapore STI ETF has rebranded to the Amova Singapore STI ETF (SGX: G3B).

When it comes to ETFs that track the STI, there are two main players. Amova Singapore STI ETF vs SPDR STI ETF

While they both aim to mirror the same 30 stocks, there are subtle differences in their operation. Here is how they compare:

A Closer Look at the Differences

Management Fees and Expenses

The Amova STI ETF has significantly reduced its management fee to 0.09% per annum as of October 2025, making it the lower-cost option compared to the SPDR STI ETF.

Tracking Difference

This measures how closely the ETF follows the index it is tracking. Both the SPDR STI ETF and the Nikko AM Singapore STI ETF are physically replicated, meaning they actually own the shares of the companies in the STI. Because of this, both funds track the index with very high accuracy. You will not find a significant difference in returns here.

Assets Under Management (AUM)

The SPDR STI ETF is the older, larger fund. A higher AUM is generally seen as a sign of fund stability and liquidity, though for a major index like the STI, both funds are more than large enough to ensure you can buy and sell units without issues.

Dividend Yield

The dividend yield for both funds typically tracks the underlying index's yield. Since both contain the same 30 stocks, the payouts are essentially mirrors of one another. If you are looking for passive income, both are equally capable tools for your portfolio.

A Practical Guide to Investing in the STI ETF

Investing in these ETFs is straightforward. You essentially treat them like buying any other stock on the SGX.

Step 1: Open a Central Depository (CDP) Account

If you want to hold your shares directly, you need a CDP account. This is where your shares are safely stored. Most local bank trading apps will prompt you to link this when you open a brokerage account.

Step 2: Choose Your Brokerage

You can use a local bank's brokerage platform (like DBS Vickers, OCBC Securities, or UOB Kay Hian) or a modern online broker that supports SGX trading.

Step 3: Fund Your Account and Place an Order

Once your account is ready, transfer your funds. Search for the ticker symbol ES3 or G3B in your app. Decide on the number of units you want to purchase and hit buy.

Another way is to instruct your bank to set up a Regular Savings Plan. It is a disciplined investment method that uses Dollar-Cost Averaging (DCA).

Instead of investing a massive lump sum, you set aside a fixed amount of money (e.g., $50 to $100) to invest automatically at regular intervals into the STI ETF.

Remember: The minimum lot size on SGX is usually 100 units.

Wait, How Do I Choose?

If you are a beginner, the most important thing is the commission fees charged by your broker. Some brokers charge a minimum fee per trade, which can eat into your profits if you are only investing small amounts every month. Look for brokers that offer low-cost regular savings plans (RSP) for these ETFs.

The Verdict: Is It Worth It?

Investing in the STI ETF is a classic "income" strategy. You are buying for stability and dividends rather than explosive capital appreciation.

If you are young and hungry for growth, the STI might feel a bit too slow for your liking. However, for a balanced portfolio, it serves as a wonderful bedrock. It provides exposure to the pillars of our economy and pays out consistent dividends that you can reinvest to harness the power of compounding.

Final thought: Investing is a marathon, not a sprint. Whether you choose the STI or global indices, the most important thing is to start early and stay consistent. Don't worry about trying to time the market perfectly. Simply, focus on building your wealth one unit at a time. Sometimes, it's the small luxuries that keep us sane, but consistently investing in your future is what will keep you secure.