Gen Z: You Will Probably Need To Be Earning $9,270 per Month in Order To Retire by 55 Years Old

%20(1).png)

With the cost of living rising faster than the humidity on a rainy afternoon in Yishun, it is no wonder that some of us are choosing to exit the rat race and "lie flat". Gen Z is facing a difficult financial landscape. One which their parents will not be equipped to guide them on either.

We have all been there, staring at a $7 McSpicy meal and wondering if we should have just stuck to a $4.50 plate of chicken rice to save up for that next life milestone purchase.

Born Between 1997 to 2012

If you were born between 1997 and 2012, you are part of a generation that is often called "strawberries" by the older folks, but the truth is that you are navigating one of the most expensive eras in Singapore’s history.

Retiring at the age of 55 sounds like a dream, but is it still actually doable?

To find out, we have crunched the numbers, accounted for inflation, and looked at the cold, hard data of HDB prices.

TL;DR: The Golden Number for Gen Z

- The Goal: Retire at age 55 with a basic standard of living (adjusted for inflation).

- The Strategy: Follow the 50/30/20 rule (50 per cent expenses, 30 per cent investment at 1.99 per cent return, 20 per cent savings).

- Housing Reality: Expect HDB prices in 11 years to be roughly 1.4 times higher than today’s already tear-jerking resale prices.

- The Verdict: Depending on your birth year, you need to earn between $6,800 and $11,500 per month on average throughout your career to retire by 55-year-old.

Inflation: Why $1,379 per Month Will No Longer Be Enough

The Lee Kuan Yew School of Public Policy (LKYSPP) states that a single senior in Singapore needs at least $1,379 per month for basic needs. That was in the year 2019. The good news from the report is that, if you are married, you will require lesser per person (couple elderly household requires $2,351 per month).

The amount is not just on basic necessaities, but it includes things like a modest annual holiday, and even the occasional treat for the grandkids.

But here is the catch: we need to factor in infltion

By the time a Gen Z born in 2012 reaches age 55 in the year 2067, that $1,379 will feel like spare change.

Using an average long-term inflation rate of 2.5 per cent (a conservative estimate based on Singapore's historical headline inflation), here is how much you will actually need to sustain that same lifestyle when you hit 55.

Basic Monthly Needs Adjusted for Inflation

Note: Calculations based on a 2.5 per cent CAGR from the 2019 baseline of $1,379.

That Roof Over Your Head

You cannot talk about retirement without having a proper roof over your head.

Staying in a tent at East Coast Park is not a sound retirement plan.

For most Singaporeans, our home is our biggest asset. Unfortunately, it is also our biggest liability during our working years.

If you are a younger Gen Z (born in 2012), you will likely be entering the property market in about 11 years. We have estimated current resale prices across various towns and projected them into 2037 using a 3 per cent annual growth rate.

It is "sian" to think about, but waiting too long might cost you more than just time.

HDB Average Prices (Now vs 11 Years Later)

Projected prices assume a 3% annual appreciation rate, price of HDB resale flats are projected to increase by 3-6% per annum.

More Math to Retiring By 55

To retire by 55, we are going to assume a strict 50/30/20 budget rule:

- 50 % of Salary on Daily Expenses. Rent/Mortgage, food, transport, and that Netflix subscription.

- 30% of Salary on Investment. Put this into a risk-free or low-risk instrument (like the CPF OA or a very stable bond) yielding 1.99 per cent per annum.

- 20% of Salary Goes into Savings. This goes into a high-interest savings account (which we will assume at 0 per cent real return for the sake of simplicity and safety).

Your Retirement Pot at age 55 = Total investment principal + Total returns earned from investment + Total accumulated savings

The average lifespan of a typical Singaporean is about 83.5 years old. Taking into account the advancement in technology, we expect Singaporeans to live longer in future. Hence, we will assume an increased lifespan of age 85.

To live from retirement age 55 to age 85, that will be 30 years of retirement. you need a nest egg that can generate the monthly income shown in Table 1.

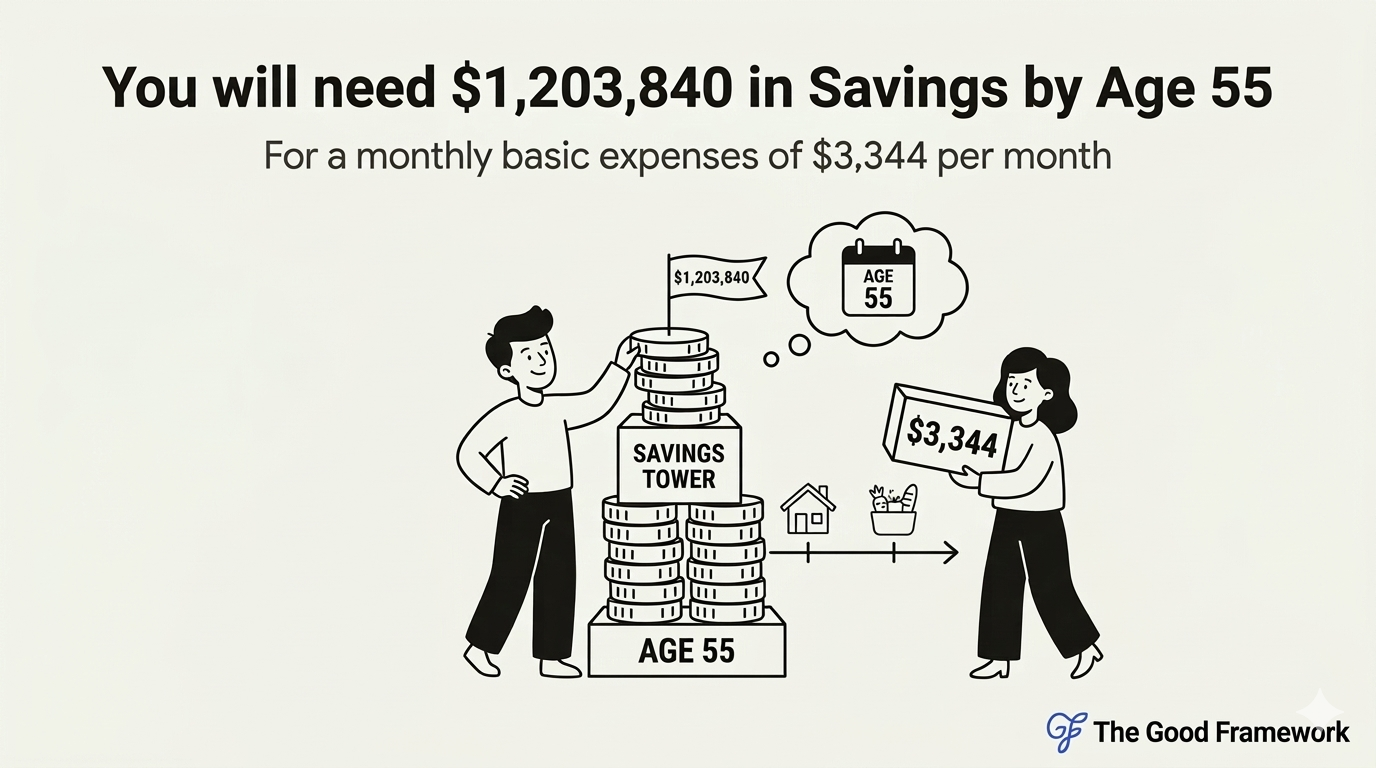

The Math Behind the Magic Number: You Need $1,203,840 to Retire

Taking a Gen Z born in 2000 for example. In 2026, they are 26 years old.

They have 29 years until they turn 55.

They need $3,344 per month in retirement.

Assuming that they have a house that is fully paid for. We are also going to exclude the potential monthly payout from CPF in this case.

Total retirement fund required: $3,344 x 12 months x 30 years = $1,203,840

To reach this $1.2 million goal in 29 years using the 50/30/20 rule, they need to earn a consistent monthly salary that allows their 30% investment and 20% savings to grow into that amount.

How Much You Need to Earn?

This is the table you came for. This is the average monthly salary you should aim to earn from now until you hit 55 if you want to call it quits and enjoy your golden years early.

Monthly Income Needed to Retire by 55

Assumes retirement from age 55 to 85. Total Nest Egg Needed is (Monthly Need at 55 x 12 months x 30 years).

Is This Salary Realistic?

Without sugarcoating, looking at these numbers, anyone would feel intimidated.

Do take note that the $9,270 monthly figure is the average across your entire career.

As you get older, your salary usually increases. Your starting pay might be $4,000, but by age 45, you could be earning $15,000.

However, there are a few ways to lower these requirements:

- Invest More Aggressively: The 1.99 per cent return we used is very safe. You should be looking at how to generate more income from making sound investment.

- Delay Retirement: Retiring at 65 instead of 55 gives you 10 more years of compounding and 10 fewer years of retirement to fund.

Final Thought: Live Your Best Life

Personal finance is personal. Ultimately it is your life, so live it. Financial planning should not be about depriving yourself of every joy until you are 55.

If you want that $7 coffee, go get it! But, maybe don't buy it every single day.

If you want to retire early, you just have to be a bit more disciplined with money.

While it is the small luxuries that keep us sane, it is the big decisions, like how much you invest, that actually set you free.